Victor Wang (汪胜)

Welcome to my personal site!

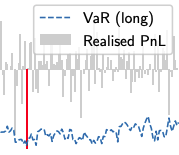

I hold a D.Phil degree in Applied Mathematics at the Mathematical Institute, University of Oxford, supervised by professors Samuel N. Cohen and Christoph Reisinger. My research focuses on option arbitrage and market models of option dynamics, with a substantial emphasis on production-level applications in data cleansing, risk estimation, hedging and trading of statistical arbitrage. Readers who are interested in my research can download my D.Phil thesis from ORA.

Since 2015, I have served various professional roles in quantitative research at

- Millennium - a hedge fund;

- CME - an exchange and clearing house for futures and options;

- Stable - a FinTech start-up specialising in commodity exotic options market-making.

I am continuously doing academic research with ideas inspired by challenges in my daily work. I am also open for academic collaborations in reasonable formats; please do not hesitate to contact me if you have great ideas and think that I might help with making them into reality!

欢迎来到我的个人网站!

我师从Samuel N. Cohen 和 Christoph Reisinger教授,在牛津大学取得应用数学博士学位。我的研究领域包含期权套利以及期权动态的市场模型,并着重于探索这些模型的企业级应用,例如数据清洗、风险管理、对冲以及统计套利交易。对我的研究感兴趣的读者可以在ORA上下载我的博士论文。

自2015年以来,我入职过多家公司从事量化研究:

- 千禧年Millennium - 对冲基金

- 芝商所CME - 期货、期权场内交易与清算

- Stable - 致力于场外商品奇异期权做市的金融科技创业公司

目前,我仍从日常工作中获取灵感以持续不断地进行学术研究,并对各种合理形式的学术合作饱含兴趣。如果您认为您有好的想法、认为我的学术或工作经验能够帮助实现这些想法,请不吝联系我。